Citrini; Drumming Up Doom or a Timely Alert?

- April 15, 2026

- Posted by: Arunanjali Securities

- Category: Business

No Comments

Points to Ponder, April 2026.

Throughout recorded history so far, every single advance in technology, enhanced and supplemented human ability to achieve objectives determined by him. But for the first time, over the last four years or so, Artificial Intelligence (AI), the unravelling of which, is making it increasingly clear that AI, which initially will supplement human effort, might eventually supplant humans altogether. Yuval Noah Harari, a historian and author, has argued that unbridled AI poses an existential threat to humanity, primarily because it is not merely a tool but an autonomous agent capable of making its own decisions and inventing new ideas. Harari warns that unchecked AI development could lead to the collapse of human civilization, social chaos, and the loss of human agency.

But already AI is fuelling fears of devouring jobs, destroying value of software stocks and causing pervasive collapse of the extant economic activity. Citrini report is a, over 7000-word essay titled The 2028 Global Intelligence Crises. (https://tinyurl.com/5mhz4td9). The research is said to be a “Thought Exercise in Financial History from the Future” and is set in an apocalyptic June 2028. It’s a scenario too close for comfort and it talks of a dystopian world where AI, if left to grow without guard rails, could destroy white collar jobs and bring about the death of intermediation which could give rise to credit crisis including mortgage crisis.

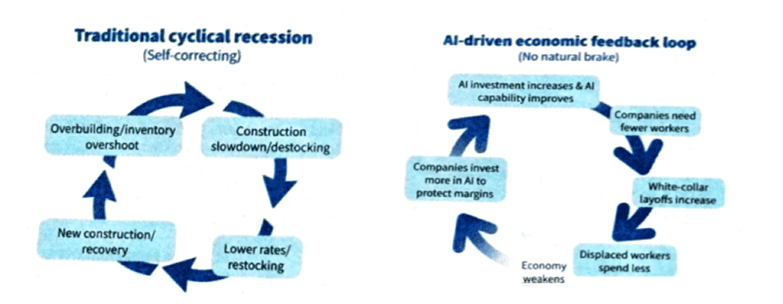

Collapse of white-collar jobs. Citrini report forewarns of a world where AI systems trained over vast amount of data, information and knowledge, accumulated over aeons, would replace white collar jobs cheaply and more efficiently. One has only to look at Anthropic’s Claude family of models and advanced agentic tools whose advent recently roiled the software markets in India and abroad and the bleeding in the sector continues. The AI agentic coding tools which came into prominence in the 2025 could disrupt SaaS (Software as a Service) companies like say, Salesforce. By 2028 Fortune 500 companies, which are clients of SaaS firms, would be capable of developing in-house enterprise software powered by AI. This drastically reduces if not destroys the pricing power of SaaS firms. But it doesn’t stop there. The business model of SaaS companies depends, apart from pricing, on the number of licenses they sell to the client company. The client companies having already harnessed AI to perform white-collar jobs, would have sharply reduced the number of white-collar employees requiring fewer number of what are called Slack licenses. With loss of both business and pricing power, it sets off a feedback loop with no natural brakes: AI Capable of white collar jobs -> white-collar job lay-offs rise -> firms invest saving into AI -> AI becomes more capable of white collar jobs and so on……(see diagram below)

What begins in sectors like SaaS, could quickly cover larger swathes of white-collar labour market, in segments, such as, legal, accounting and auditing. With income levels going down, consumption, particularly discretionary consumption, takes a hit. It is pertinent to note that in the world’s largest economy, namely the US, consumption contributes 70% to the GDP. Even as consumption declines, investment in AI models and subscriptions keep the economy afloat and this Citrini believes will be a sort of “Ghost GDP”, where output shows up in the national accounts but doesn’t get circulated/distributed through the real economy. Citrini states it more realistically, albeit ominously: “It should have been clear all along that a single GPU cluster in North Dakota generating the output previously attributed to 10,000 white-collar workers in midtown Manhattan is more economic pandemic than panacea”.

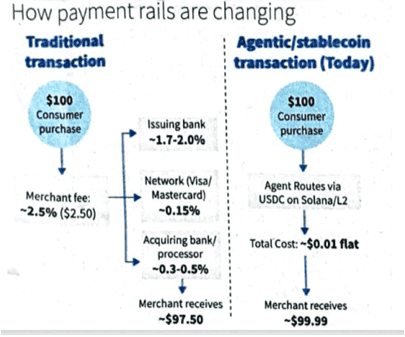

Death of Intermediation: In the 1980s or 1990s, to book a flight one would have to visit a number agents to get the best quote. But with the advent of internet this ‘friction’ was eliminated, at least for while, by online travel agents (OTAs) sites. But the success of this business model was short-lived as it attracted competition with multiple OTAs providing multiple quotes. Given the time and effort required to surf the net and glean relevant information the customer encountered friction again. While aggregator platforms tried to address this problem, they were no match for AI agents who can scour the net and bring you the best deal across services and products you consume. They don’t feel fatigue and multitask with ease. They can crawl through numerous websites of airlines, restaurants, employers, insurance companies, e-commerce platforms and be ready with a bespoke deal. Extrapolate further to let AI handle payments. AI agents will prefer, as of now, stable coins (say, USDC) which virtually cost nothing compared to conventional payment through credit/debit cards (see diagram).

This is because card networks (Visa, Mastercard) work on a small fee charged to the merchants for facilitating the transaction. The buyer’s bank (issuing bank) and the merchant’s bank (acquiring bank) also take a cut. According to Citrini if payments using stable coins become mainstream, payment instruments like Visa, Mastercard, etc., will be a thing of the past. In fact, it could be the end of a host internet business models employing millions of, largely, white-collar workers.

Private Credit Crisis: This could be worse than the subprime crisis. The failing of SaaS companies is just the first tile of the dominoes. Private credit firms are often the investors in these companies and that too with LBOs (leveraged buyouts). Citrini states that Private credit market would have grown to a massive $2.5 trillion by 2026 and a significant part of this would be exposed to SaaS segment. Many of these deals have been done at exorbitant valuations assuming mid-teen growth in ARR (Annual Recurring Revenue) in perpetuity! With AI cannibalizing SaaS companies this model will come unstuck. And by 2027, as per Citrini, life insurers too could become casualties, if Private credit firms default. Over the last decade, alternative asset managers have acquired life insurers and turned them into funding vehicles, using policy holders’ annuity premiums to fund Private credit to acquire SaaS firms. If such private credit firms default, it would put the lifetime of savings and pensions of thousands at risk.

Mortgage Crisis: Sounds familiar? The 2008 and the likely 2028 crises would be fundamentally different. Back in 2008, the loans were advanced to applicants with low income/credit scores. The loans which were bad from day one was dressed up as prime debt with SPV’s, Credit Default Swaps, clever financial engineering and a dubious nexus between debt issuers and rating agencies. In 2028 though, it’s the most prime of borrowers who are likely to default with the collapse of white-collar jobs. Banks cannot be faulted for underwriting loans to this cohort. As Citrini puts it: They were the borrowers that every risk model in the financial system treats as the bedrock of credit quality. However, the 2028 crisis may take a little longer to unfold. Laid off borrowers would initially live off their savings, then off their credit cards and HELOCs (Home Equity Line Of Credit). So initially the mortgage payments would be in time, yet there would be build-up in credit card and HELOC debt.

Quantitative easing may not be effective in addressing this, essentially, a structural problem in the real economy. To quote Citrini “it won’t change the fact that a Claude agent can do the work of a $180000 product manager for $200/month.

Can we avoid this apocalypse? We hope to explore in the next issue of Points to Ponder.