Budget 2026-27

- March 31, 2026

- Posted by: Arunanjali Securities

- Category: Business

No Comments

Little was expected of the budget this year. Corporate and personal income tax rates were reduced in the earlier budgets and reduction and rationalization of GST rates took place during the year but well before the budget. Moreover, it was a budget that faced quite a few constraints by way slackening tax revenues, sluggish private sector investments, long shadow of tariff uncertainty, weakening rupee and risks arising out of geo-political turmoil.

But the finance minister did the unexpected. She has taken a confident shot at the future; has increased capex and still managed to keep the fiscal deficit at 4.3% of GDP. It is a budget for the medium to long term. At a time when trade and investments are weaponized, the budget pushes for strategic autonomy, export promotion and digital superiority. This is translated into focus on investments in critical minerals including rare earths, semiconductors, electronic component manufacturing and AI related technologies. There is also a vision for biopharma with an outlay of Rs 10000 over five years with an aim to creating a global hub. Amidst all this the budget has recognized the imperative of sustainable growth and towards this end has allocated Rs 20000 crores over five years to support carbon capture, utilization and storage. These investments have enhanced the quality of expenditure and it is heartening to note that Central Government’s capital expenditure of Rs 12.22 lac crores has this time exceeded its net market borrowings of Rs 11.7 lac crores.

But the budget does leave some pockets of anxiety in its wake.

- The surge in government borrowing to around Rs 17 lac crore is likely put further pressure on liquidity and consequently the overall interest rate environment could become less accommodative, especially for corporates and sub-sovereign entities as the market digests the larger of supply of bonds. This again might dampen investments, particularly for MSMEs and mid-size corporates. But the consequences of progressively increasing debt pile, are more serious.

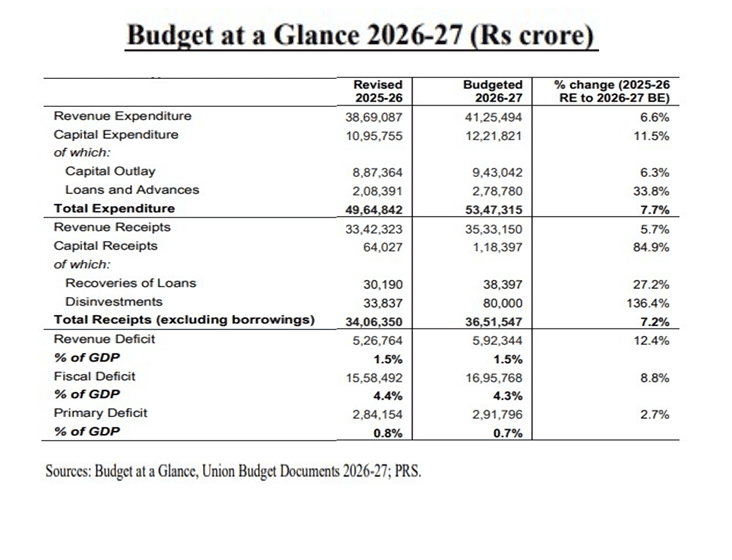

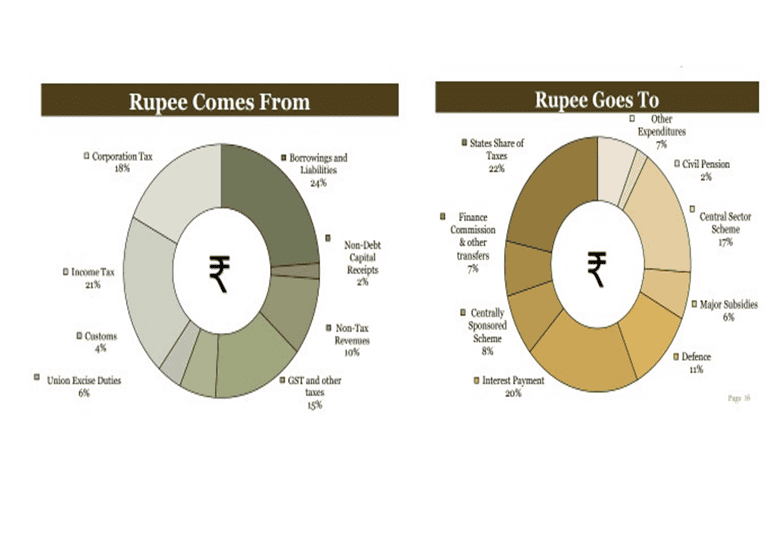

- The interest payments for FY27 are estimated at Rs 14 lac crores as against Rs 12.7 lac crores during FY 26. The climbing interest payments are a nagging worry. Barring states’ share of taxes, interest payments constitute single largest payment at 20% on the expenditure side of the budget (Cf. Annexure 1). The primary deficit, which is obtained by deducting interest payments from the fiscal deficit, for FY 27 is not even able to cover the revenue deficit (Cf. Annexure 2). This means that the government has to borrow even to meet its consumption expenditure. By this yardstick, India is on the brink of a debt trap, unless the massive capital investments made so far produce accelerated returns. The government, it appears, lives on hope and overdraft; more on overdraft than hope at the moment. What we really need is an outcome budget more than an allocation budget.

- Even the much-touted fiscal consolidation doesn’t seem to rest on firm ground. Non tax revenues budgeted at around Rs 6.7 lac crores (19% of the total revenue) is increasingly drawn from dividends and profits from public sector enterprises and the RBI, indicating an overdependence on contingent (on state of financial markets) inflows.

- After the regulatory onslaught, the budget has sharply increased STT on futures & options (F&O) in the hope that it will curb speculative activity, especially amid high retail involvement and increasing leverage. The justification is based on the premise that derivative trading is driven more by momentum than hedging or arbitration and has only increased volatility without strengthening capital formation. But to the extent the F&O market enhances liquidity and hence price discovery, experts opine that singling out F&O segment for discriminatory tax treatment betrays “nanny” orthodoxy of conventional bureaucrats. No less an economist than Arvind Virmani a member of the Niti Ayog has stated that discouraging F&O activity through tax is “throwing sand in the wheels”. More justifiably this move could have ideally been combined with reduction/even abolition of STT on equity cash market, which supports formation of risk capital and long-term ownership. In fact, with STT continuing, there is a case for elimination of capital gains tax altogether. In any case, capital gains tax could be eliminated on all sale of equities/equity related investments which are held for at least three years. Since much of the short-term trading happens within three years, this move is likely to be revenue neutral while at the same time incentivizing patient, long-term investment.

- The Union Budget 2026-27 allocated ₹1.39 lakh crore to education, marking an 8.27% increase over the previous year. While this represents a record high in nominal terms, experts consider it inadequate to meet the 6% of GDP target set by the National Education Policy (NEP) 2020. The focus is on higher education, including new university townships, but overall spending remains below global benchmarks.

The RBI, groups states based on share of population aged 60 and above. Youthful states are those with share of population which is above 60 is below 10%, intermediate states are those with share of 10-15% and those above 15% are ageing states. Each group of states require a differentiated education policy. Youthful states need to invest aggressively in human capital to absorb future labour market entrants, while ageing states must balance social security needs with productivity enhancing expenditure. The Budget doesn’t attempt to meet these differentiated needs through incentives or otherwise. This is essential if we are to realize the much-hyped demographic dividend.

Annexure 1

Annexure 2.