IPO Frenzy – Three Day Circus Or, Sign of a Mature Market?

- February 17, 2026

- Posted by: Arunanjali Securities

- Category: Business

No Comments

The last couple of years have witnessed record level of IPOs both in terms of numbers and aggregate funds raised. Fundraising through mainboard IPOs surged from ₹67,562 crore in FY 2023 to a record ₹1,82,460 crore in FY 2024, an increase of over 170%. Calendar year 2025 further saw approximately ₹1.95 lac crores raised across 373 issues, including both mainboard and SME listings. This remarkable performance has positioned India as the global leader in terms of number of IPOs. In fact, in just five years (CY 2021-25), IPOs have raised more money than they have in the previous three decades. The pipeline for 2026 also seems promising with Nearly 200 companies, including big names like NSE, Reliance Jio and Manipal Hospitals, either holding SEBI approval or awaiting clearance, collectively targeting more than Rs 2.6 lac crores. In addition, several new-age technology companies are preparing to file draft offer documents.

There are many positive features to the IPO boom that is currently underway.

Global Dominance: India consistently led the world in the sheer number of IPOs, accounting for nearly one-fifth of global volume in 2025.

Rise of Retail Investors: A significant surge in domestic retail and institutional investor participation has been a key driver, ensuring robust demand and high oversubscription rates (averaging nearly 27 times over the past two years).

SME Boom: Small and Medium Enterprises (SMEs) experienced a substantial increase in activity, more than doubling their average IPO size and contributing significantly to the overall number of listings.

Sectoral Diversity: While initial years were dominated by a few sectors like BFSI and Healthcare, the last two years have seen a broader range of industries access the public markets, including automobiles, telecom, capital goods, and e-commerce.

Enduring Performance: “In the past, a strong IPO year was almost always followed by a lull of two to three years. This time, that pattern has been broken,” said Pranav Haldea, managing director of PRIME Database Group. “If valuation discipline is maintained and the secondary market remains stable, even if not bullish, the coming years could still be a golden phase for India’s IPO market,” Haldea said.

Institutions step up, mutual funds overtake FPIs: Institutional participation remained robust. Qualified institutional buyers, including anchor investors, accounted for 62 percent of total IPO subscriptions. For the first time, mutual funds overtook foreign portfolio investors (FPIs) as anchor investors.

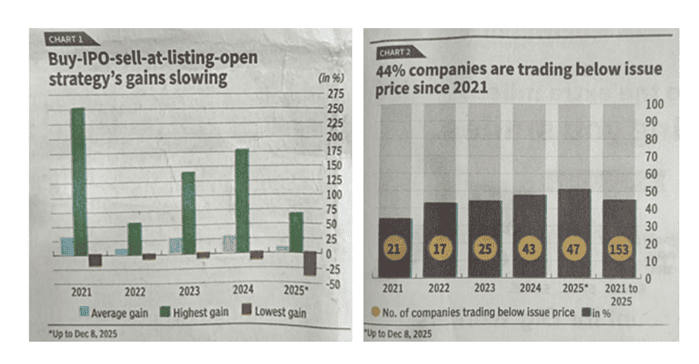

Yet serious investors and even policymakers look askance at the prevailing IPO boom. Chief Economic Adviser Anantha Nageeswaran has criticised the use of IPOs as exit route rather than for fund raising resulting in capital formation. Seasoned market watchers note that at the retail level, IPOs have become a three-day circus. Scour the grey market chatter, wait for day three subscription cues, apply for one or two lots and if allotment arrives, sell at the opening tick at 10 am. This, the experts feel is queue management with a demat account but certainly not investment! This is a process where scanning grey market and monitoring level of institutional subscription goes for due diligence and at least, at the moment, the IPO game seems to reward punting more than holding, which by encouraging excessive short-termism has diluted the desirable culture of long-term investment. But over the years the listing day gains have clearly decelerated and the patient investor would have observed that there is a good chance that IPO stocks would be available at a cheaper price post listing since 44% of companies are trading below the issue price since 2021. See Charts 1 & 2 below.

It is worth recalling Buffets warning: “you don’t want to get onto a stupid game just because it is available”. It’s a game where sellers choose the timing, hype does the marketing and buyers supply the liquidity.

But one can play the devil’s advocate with a macro perspective. While Mr Nageeswaran’s comment that using IPOs as exit route defeats the purpose of the capital markets as mobilisers of “high powered” capital to facilitate capital formation appears, prima facie valid, since nearly two thirds of the capital raised was by way of “offer for sale”(OFS). But his comment seems facile as it skirts the issue that risk capital cannot be mobilised unless there is a system to reward providers of seed capital and risk takers. The IPO market provides such a mechanism, not only by enabling risk transfer but also by rewarding risk takers with transfer of ownership through price discovery. This is achieved through rule bound transfer of securitised instruments usually from venture/private equity to diversified public holders. In fact, the Government that Mr. Nageeswaran represents, has frequently and rightly resorted to OFS, among other things, to finance its fresh capital expenditure.

It is also true that the scale at which such exits of initial risk capital providers has taken place, is possible only in a deep and mature market and that would mean that Indian capital markets have come of age. This in turn is quite likely to encourage more venture capital and private equity providers to invest in India as it holds out credible promise of profitable exit. This indeed can turn into a virtuous cycle. This is not a sign of fragility but of an ecosystem confident enough to recycle capital quickly.

A 2024 SEBI study found that 54% of the IPO shares allotted to non-anchor investors were sold within a week. One doesn’t have to revisit Hegelian Dialectics to appreciate that every phenomenon has two ways of interpreting it. One can regard this short-term trading in IPOs as froth or as market efficiently testing and allowing a churn that over time helps ownership migrate to stronger hands. As already pointed out by the charts above, the patient investor is likely to get same IPO shares much cheaper at a later date. Recent numbers show that less than half of 2025’s IPOs delivered listing day gains even as many of them quickly cooled subsequently. The moderation in listing day pops hopefully implies that bankers and issuers are readying books more carefully. Cheap money era habits, such as overtight pricing, momentum allocation, among others are fading. This may be regarded as better price discovery and governance signals.

The IPO exuberance has not only made primary pipeline bigger but also broader as is evidenced by the increasing number of SMEs listing on NSE Emerge or on BSE SME platforms. Needless to say, that SME listings are crucial to diversify the opportunity set and widen the investor base beyond large caps. Simultaneously SEBI’s efforts to tighten disclosures, emphasise profitable paths before fixing the price bands and calibrate offer sizes should provide greater depth and viability to the market.

Finally, India’s trading infrastructure and participation have over the years scaled dramatically. Even with periodic dips, exchange data show high, persistent turnover and robust derivative hedging tools. The depth allows founders’ and/or venture capital/PE players’ exits to be staged without destabilising the float. This again is a hallmark of a market that has the capacity to recycle risk efficiently.